Galloping–inflation of the U.S. dollar is now becoming obvious to a growing cohort of investors. It is driven by factors on both sides of bank balance sheets, with evidence that large depositors are reducing their term deposits and increasing their instant access checking accounts. This appears to be behind the increase in M1 money supply fuelled out of a shift from the M2 statistic, which includes savings deposits.

It amounts to a hidden run against bank balance sheets. Meanwhile, increasing supply chain problems against a background of covid lockdowns are leading to the withdrawal of bank credit from non-financial businesses, potentially imploding bank balance sheets as a bank credit contracts.

Foreign support for both the dollar and dollar-denominated fixed interest assets are being withdrawn, which is sure to lead to rising bond yields and dollar interest rates in the New Year, undermining the equity market bubble

The Fed is now faced with not only financing ballooning federal budget deficits, but underwriting US supply chains in their entirety, which is corroborated by ongoing global logistical problems, tying up an annualised $34 trillion of intra-business payments in America alone. The Fed’s unwavering commitment to Keynesian monetary policies will lead the Fed to attempt to offset these supply chain problems, to rescue banks that fail to survive the inevitable contraction in bank credit, and to defray the bad debts that will arise.

It is a momentous task encompassing the whole US economy, requiring even faster “money-printing”, and is impossible without partial destruction of the unbacked U.S. dollar.

As a consequence – commodities, stocks, cryptocurrencies and precious metals were all rising because of the dollar’s loss of purchasing power.

The media is still reporting on the economic effects solely of Covid-19. In doing so, they have consistently underestimated them and ignored other factors. To return to a normality was always there as a beacon of hope — the spring of hope in a winter of despair. And it has only been a small minority who have pointed out that far from being a solution, inflationary financing has negative consequences. And even fewer of us who have tried to demonstrate that instead of stimulating economic activity, debasing the currency actually kills it.

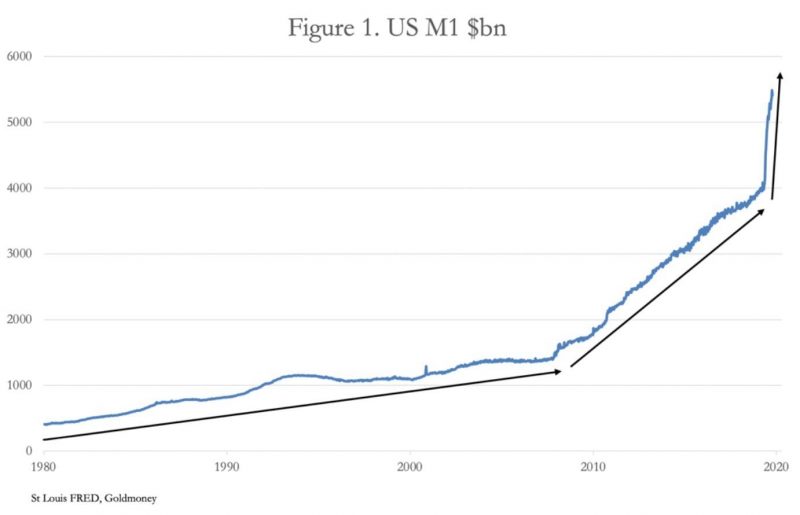

The pace of monetary destruction is making a new leap. Figure 1 is the money supply of the world’s reserve currency, which is soaring at a new pace. In the last two weeks of November, M1 money supply jumped by over 14%.

The galloping inflation or even hyperinflationary trend of U.S. M1 money supply is clear. But everyone has become so bemused by these developments that they have taken to disregarding them, while prices in stocks, commodities and cryptocurrencies console them by rising. These developments must not be ignored by anyone who wishes to preserve their wealth, and they give important clues to the road ahead.

According to the most recent figures, the sum of total checkable deposits and the currency component of M1 increased in November by $435.7bn, a rise of 11.6%, while total savings deposits fell by $88.5bn (0.75%). The difference between the former two and the latter is instant access. It represents a turnaround from rapidly increasing savings deposits between April and June, to increasing cash and checking accounts instead. It is a new trend which differs from the relationship between instant access and savings accounts at the time of cash contributions to families from the Treasury. To the extent that the helicopter-drop bolstered savings accounts, that effect has faded, and following the slowing of the rate of increase in savings deposits, total savings deposits in November actually fell for the first time this year.

The reasons for this turnaround reflect a new reluctance by depositors to tie up funds in the banking system. To be clear, with smaller depositors protected by the FDIC, the shifts in deposits are sure to be mostly in balances larger than the insured amounts of $250,000, almost certainly reflecting a financially informed class of depositor, likely to be trading in financial assets. The apparent suddenness of the change in attitude among large depositors should pique our interest.

We cannot blame zero interest rates on this development, because there were massive inflows totalling $1.24 trillion into total savings deposits in March April and May, when interest rates were also zero. The most likely reason time deposits are not being renewed is because it is a first step for bank customers who intend to reduce their overall currency exposure relative to the assets, goods and services they normally buy, which for them will embrace all their bank balances, including comparatively illiquid savings accounts.

In the context of a combination of monetary inflation and the effect on asset prices, encashment of savings deposits makes sense. There is no point in lending money to the bank for zero interest, when prices of the assets and goods you buy are rising. And if you sell them, there is then no point in tying up the proceeds in time deposits — better to buy something else. Even though this change of behaviour appears to signal that the depositors concerned are increasingly aware that prices are rising, and that assets and goods should be bought sooner rather than later, they are yet to appreciate that the phenomenon is of the purchasing power of the currency falling rather than prices rising.

This gives us an indication on where we are in the hyperinflation process. The signal we are being given by the rise in money M1, including the extent that it is now fuelled out of savings deposits, is that it will eventually lead to an acceleration of the disposal of money by all bank depositors. But we are not there yet.

In the past, hyperinflations of the money quantity have led through rising prices to an increase in demand for currency in the form of notes. In the Germany of 1922—23, wage earners had to encash their salaries in order to spend them immediately, which led to a rapid increase in demand for paper marks while their purchasing power collapsed. This is why the printing presses were running at full tilt. In the modern economy where cash notes and coin play only a small role, the raising of spending liquidity at the banks creates a reservoir of funds, which when a shock comes, is poised to flow rapidly into anything which is not fiat money.

If that condition is triggered, it will drive the dollar’s purchasing power over a cliff-edge. An adjustment on these lines will lead to a more sudden increase of consumer goods prices measured in declining fiat than occurs in an economy where cash notes are the principal means of payment. But we are not there yet.

For commercial banks the initial effect of a reduction of savings accounts increases their exposure to the temporal mismatch between funding and their loan books. In the past, this has ended up with bank runs, such as that of Northern Rock in the UK in 2008, a warning of what was to come. A more apt laboratory example, perhaps, is the collapse of the whole Cypriot banking system in 2012. This is getting closer to where we are.

The assumption in financial circles is that the soft ban on cash and improved communication between banks and their regulators make bank runs a thing of the past. The trouble will lie with banking customers who have failed to get this message.

We now have a partial explanation for why, as our first chart in Figure 1 showed, M1 money is soaring, because money has been diverted from from savings deposits which are only included in the broader M2. That leaves another puzzle to solve, which is on the asset side of the banking system’s collective balance sheet.

The contraction in gross output to the mid-year point approached $4 trillion, and as we have seen, the initial response from the banks was to extend credit to alleviate the supply chain crisis. But given that annual movement of all supplies is the equivalent of gross output, the implication of the initial increase in bank lending to end-June was the banks loaned credit of an extra $1.6 trillion, and the non-financial sector (i.e. the basic economy) absorbed supply chain costs of $2.3 trillion, leaving business finances very stretched.

The situation has deteriorated further since end-June. As they breathe in and count up to ten, bankers now realise that the Fed has not done enough to protect them from the true scale of the logistics disaster. Unlike Lehman, which they rode through, they are now fully exposed to a rapidly deteriorating situation. They can no longer afford to support cash-strapped businesses while the Fed dithers, which is why the sudden collapse in bank lending is now taking place and appears to have much further to go. And seeing their depositors withdrawing term lending, commercial banks are now in a growing panic to rein in their bank lending and de-gear their balance sheets.

The Fed’s mounting tasks

So far, the Fed has been acting conventionally in Keynesian terms to rescue the US economy. In order to ensure that the consequences of covid are contained, it has promised unlimited QE, currently running at $120bn a month, to fund the increase in the Federal budget deficit. They have imposed zero interest rates to keep funding costs down. The initial round of monetary inflation financed two-thirds of increased federal spending in the second half of fiscal 2020 to end-September, the remaining third being from revenues. A second “stimulus package” is due shortly, which will be financed by yet more monetary inflation.

The Fed’s task is now evolving from only financing the government’s ballooning deficit to backstopping supply chain disruptions as well, now that bank lending is failing to keep pace. While the former problem is still ongoing, the latter is far larger, which without the Fed’s successful intervention will end in a deflationary slump to rival the 1930s, with banks failing under the pressure from previous lending excesses and from the consequences of rising bad debts. To save the banks, they will have to be supported in the face of current and future loan commitments. And for future credit expansion, regulations will have to be amended or suspended, because the banks now lack the equity backing to expand their balance sheets sufficiently.

Even if that could be achieved, the Fed is up against the 80/20 Pareto rule, whereby roughly 80% of private sector economic activity is by local small and medium sized businesses. Getting support to SMEs is a mammoth task, and merely supporting supply chain payment flows, substantial though they are, will not be sufficient to resolve mounting economic problems for smaller businesses. But having embarked on a Keynesian solution to everything, for the Fed there can be no turning back, and anyway they have no mandate to do so. The stimuli for covid are becoming small beer compared with what the Fed has yet to face.

The growing realisation in the banking community that America and the wider world faces a deep economic slump will do what these conditions are bound to do — lead the banks into a race for the exit. Reassurances from the Fed will not stop it. Foreigners, with over $6 trillion of bank deposits and $22 trillion of financial assets in American dollars will also race for the exit by selling dollars for other currencies, commodities and gold — anything but dollars. This is already happening as Figure 3 of the dollar’s trade-weighted index shows.

Domestic depositors, faced with the choice of being creditors of any bank (moving funds from one to another is no solution for systemic issues) will increasingly opt to exchange their swollen bank accounts for anything but dollars in the bank, leading to a crack-up boom.

One factor not seen in previous monetary collapses is that there is now an educated class of cryptocurrency fans, who understand that the Fed’s monetary policy is causing the dollar to collapse, relative to their favoured cryptocurrency. Their education is far from complete, but that doesn’t matter. They are making money, measured in fiat, and everyone sees it. Gone is the situation where only one man in a million understands what is happening to money. This can only quicken the pace of the dollar’s collapse.

The choice between financial assets and other goods

So far, we have detected that depositors not protected by the FDIC have been liquidating their savings deposits in favour of cash in order to invest in inflating assets. For every asset bought, there is a seller who banks the proceeds. And with cryptocurrencies, equities, commodities and raw material prices all in bull markets, sellers are reinvesting instead of just taking profits. Clearly, this activity is being driven by increasing speculation in market bubbles, and to a minimal extent by fear of the dollar losing its purchasing power for tangible goods. For evidence that this is not yet an inflation trade, we only need to look at market sentiment for gold, whose performance has noticeably lagged that of other financial assets.

In the absence of a widespread fear of currency debasement, we must conclude that the actions in financial markets, with the exception of fixed interest where there is only one buyer — the Fed, are indeed speculative bubbles, and that these bubbles will burst. When bubbles go pop, money which exists only in valuations simply disappears.

An important consequence is that bank collateral, which is increasingly in the form of listed financial assets or those that relate to them, falls in value, exposing the folly of excessive balance sheet leverage by leaving loans inadequately covered. The bank collateral problem was expressed by Irving Fisher in his analysis of the Wall Street Crash and how that led to self-feeding losses at the banks. Nothing needs to be added to his description.

Without the Fed’s intervention, a reduction in the availability of bank credit will lead to sharply higher borrowing rates due to increasing refinancing demands at a time of credit contraction. Interest rates are far too low on this account alone. Historically, the conditions that lead to speculative bubbles imploding are nearly always related to rising interest rates and bond yields, exposing malinvestments.

The consequences of a falling currency over-owned by foreign interests can also trigger these conditions. For foreign investors the returns on dollar-denominated assets are struck after currency losses, and this is particularly noticeable in fixed interest, where yields are far too low to offset the currency losses now arising. According to US treasury TIC figures, in the last twelve months to October private sector foreigners have liquidated nearly $300bn of fixed interest Treasury bonds, corporate and agency bonds. The true liquidation is larger once offshore dollar-based captive insurance businesses are removed from the figures.

The underlying condition is of time preference, which, in a falling currency, alerts foreign owners to future losses not offset by current interest rates. This is why capital gains from falling interest rates to offset the lack of interest income have become so important for foreigner investors. But as Figure 4 shows, with rising yields there is a growing sense that profits from falling yields will now be replaced by capital losses from rising yields.

Rising bond yields for US Treasury debt have further negative implications for equity markets. Valuations are solely based on the Fed’s monetary policy and completely divorced from the prospects for business in the non-financial sector, where supply chains are failing and bankruptcies mounting.

Bank depositors holding in excess of the FDIC $250,000 limit on protection will attempt to reverse their current bullishness on equities by liquidating their positions. The traditional safe-haven attractions of swapping bank deposits for US Treasuries will be swapping creditor status at insolvent banks for collapsing bond prices in a collapsing currency. The only refuge is likely to become a choice between precious metals and cryptocurrencies, in an attempt to rid themselves of dollars.

Developments on these lines are repeating the experience of the John Law episode in France exactly three hundred years ago. Wise bankers, such as Richard Cantillon, played the bubble collapse not by shorting the Mississippi venture, but Law’s paper currency, the unbacked livre, on the foreign exchanges in London and Amsterdam in return for currencies backed by gold and silver. That was the second fortune he made from Law’s paleo-Keynesian policies, the first from secretly selling Mississippi shares deposited with him as collateral.

There can be little doubt that the monetary, banking and economic developments and their requirements for an additional and unlimited expansion in the money supply is set to destroy the dollar and all the fiat currencies that take their cue from it, as surely as John Law’s currency collapsed three hundred years ago. In their partial understanding of what represents money, the cryptocurrency community are just the first to get this message.